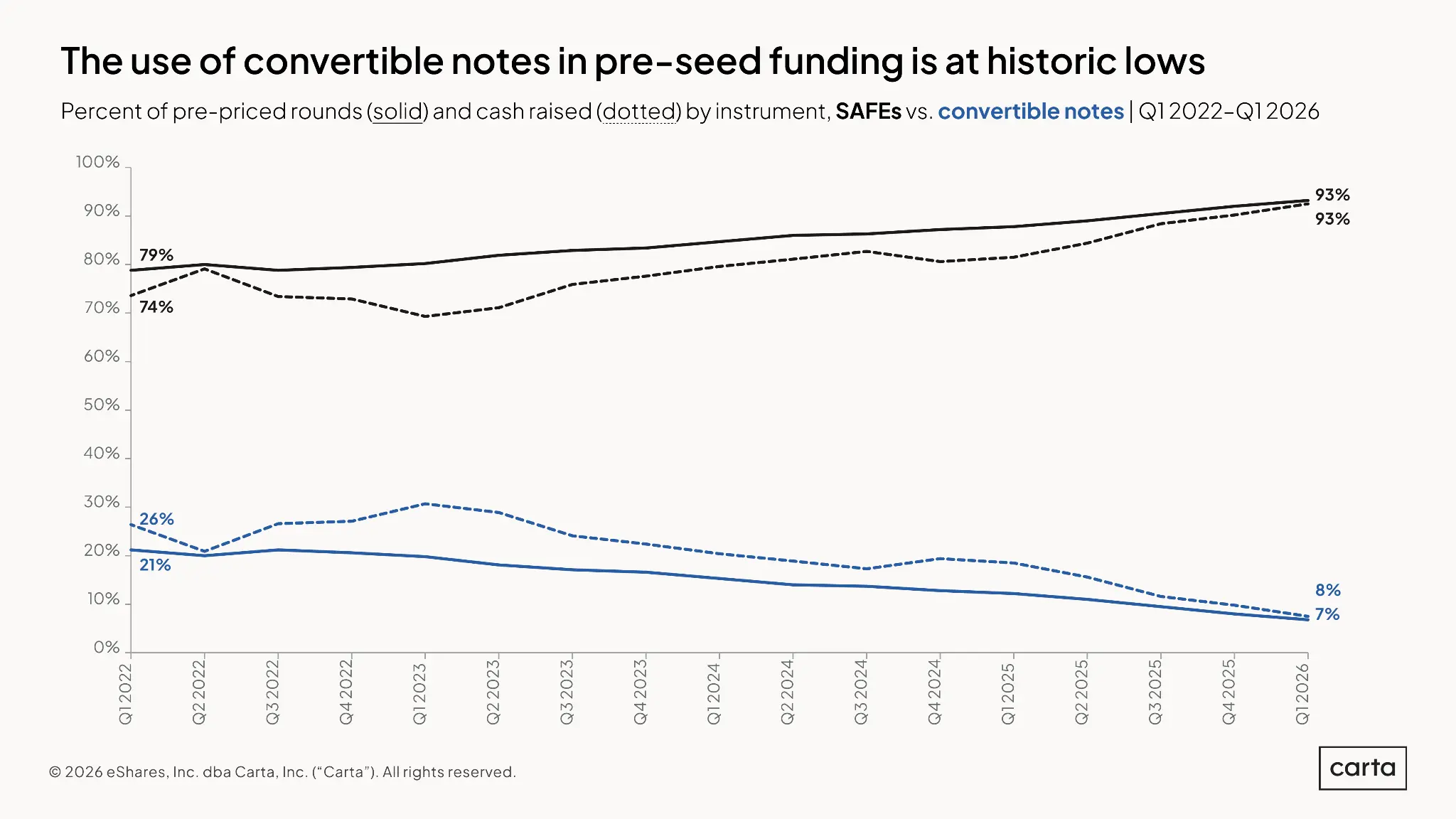

According to Carta, SAFE notes are now being used for 93% of pre-priced rounds (i.e. pre-seed and seed rounds), more than 14x more frequently than the traditional convertible note (CN) structure. That's pretty impressive when you consider that SAFEs didn't even exist before 2013. This shift is driven by several key advantages that SAFEs offer over traditional CNs, making them more attractive for early-stage fundraising. This is especially true for rounds under $2M in size. Let's explore why.

If you don't know what Qualified Small Business Stock (QSBS) is, I suggest reading this article first. In a nutshell, QSBS (IRC §1202) was created by Congress to incentivize investments in early stage companies. After enhancements that were included in the One Big Beautiful Bill Act (OBBBA) on July 4, 2025, QSBS now offers investors tax-free capital gains on the first $15M or up to 10x of the investment amount, whichever is greater. With the caveat being that the IRS has not yet officially opined on whether SAFEs count as "pseudo equity" or not, the latest version of the Y-Combinator SAFE Note includes language to support its treatment as an equity, thus potentially being more likely to be treated that way. Unfortunately, even though a dozen years have passed since the creation of SAFEs, the IRS has yet to publish any sort of official determination.

There are features that can be added to a SAFE note, however, that can help tilt the fact set over to the QSBS-qualification side, such as adding an optional conversion to Common Stock at a predetermined post-money valuation, by a majority vote of the SAFE holders, should a Preferred Stock (i.e. priced round) not materialize within a certain period of time. Many people are not aware that SAFEs are a boilderplate that can be modified, just like convertible notes can. This is even more important now that Congress is has added multiple enhancements to the QSBS tax exclusion rules. Our favorite version, of course, is the Venture Mechanics SAFE Template.

SAFE notes are designed to be straightforward and quick to execute. They eliminate the need to negotiate interest rates, maturity dates, and repayment terms, and other provisions which are common in convertible notes. This streamlined process reduces legal costs and accelerates fundraising, a critical advantage for startups looking to move fast. Unmodified SAFE notes can literally be downloaded from YC. Convertible notes require an experienced corporate securities attorney to draft, as some significant cost. SAFE notes can also be amended by an attorney to include features that might help the offering appeal to more investors, such as optional conversion to Common Stock at a fixed valuation should a priced round not happen within a specific period of time, such as is featured in the Venture Mechanics SAFE Template.

Unlike convertible notes, SAFEs are not loans and thus do not carry debt on the company’s balance sheet. They do not accrue interest and have no maturity date, freeing startups from the pressure of repayment deadlines or accumulating liabilities. This financial flexibility allows founders to focus on growth rather than debt management.

The fact is that even though virtually all CNs have provisions for investors to be paid back in part or in whole should the company fail, as the saying goes, "there's no such thing as a debt investment in a startup," because the incidence of this actually occurring is extremely rare. When startups fail because they were unable to raise their next round, there usually isn't enough money left to distribute out to investors after the expenses of bankruptcy or dissolution. There is a common misconception that because SAFEs aren't debt, investors have no way of recovering their money in case the business shutters. But this is likely to be the case 99% of the time anyway, so they might as well take advantage of SAFE notes' other attributes such as potential qualification for QSBS tax treatment.

SAFE notes convert automatically into equity during the next priced equity financing round, typically at a valuation cap or discount agreed upon at issuance. This automatic conversion simplifies the transition from early-stage funding to equity ownership without complex triggers or negotiations that convertible notes sometimes require.

SAFE notes are usually based on standardized templates that minimize negotiation and documentation. Convertible notes often require separate purchase agreements and more extensive legal review due to their debt nature and additional terms like interest and maturity provisions. Smart investors will typically have a qualified CPA or securities attorney review those documents prior to investment, and may rack up some legal expenses on both sides before agreeing to send in their funds. It is to the benefit of both the founders and their early investors to avoid such legal expenses.

SAFEs align investor returns with the company’s success by focusing on future equity rather than debt repayment. While convertible notes offer more investor protections through interest and maturity dates, SAFEs foster a collaborative environment by removing repayment pressure and emphasizing long-term growth potential.

SAFE notes are rapidly overtaking convertible notes as the preferred instrument for pre-priced rounds because they offer a simpler, faster, and more flexible way to raise capital without the burdens of debt. Their automatic conversion, lack of maturity dates, and standardized documentation reduce legal complexities and costs, making them particularly attractive to startups eager to focus on growth. While convertible notes provide stronger investor protections through debt features, the startup ecosystem’s growing preference for agility and simplicity has propelled SAFEs to prominence as the structure of choice in early-stage fundraising. Lastly, the likelihood that SAFEs may start the 3-year clock on QSBS capital gains tax qualification sooner than convertible notes do - especially if slightly modified to include the aforementioned modifications - adds a huge additional incentive for investors to opt for SAFEs. And the proof is in the pudding in that 93% of pre-priced rounds today are done on SAFE notes.