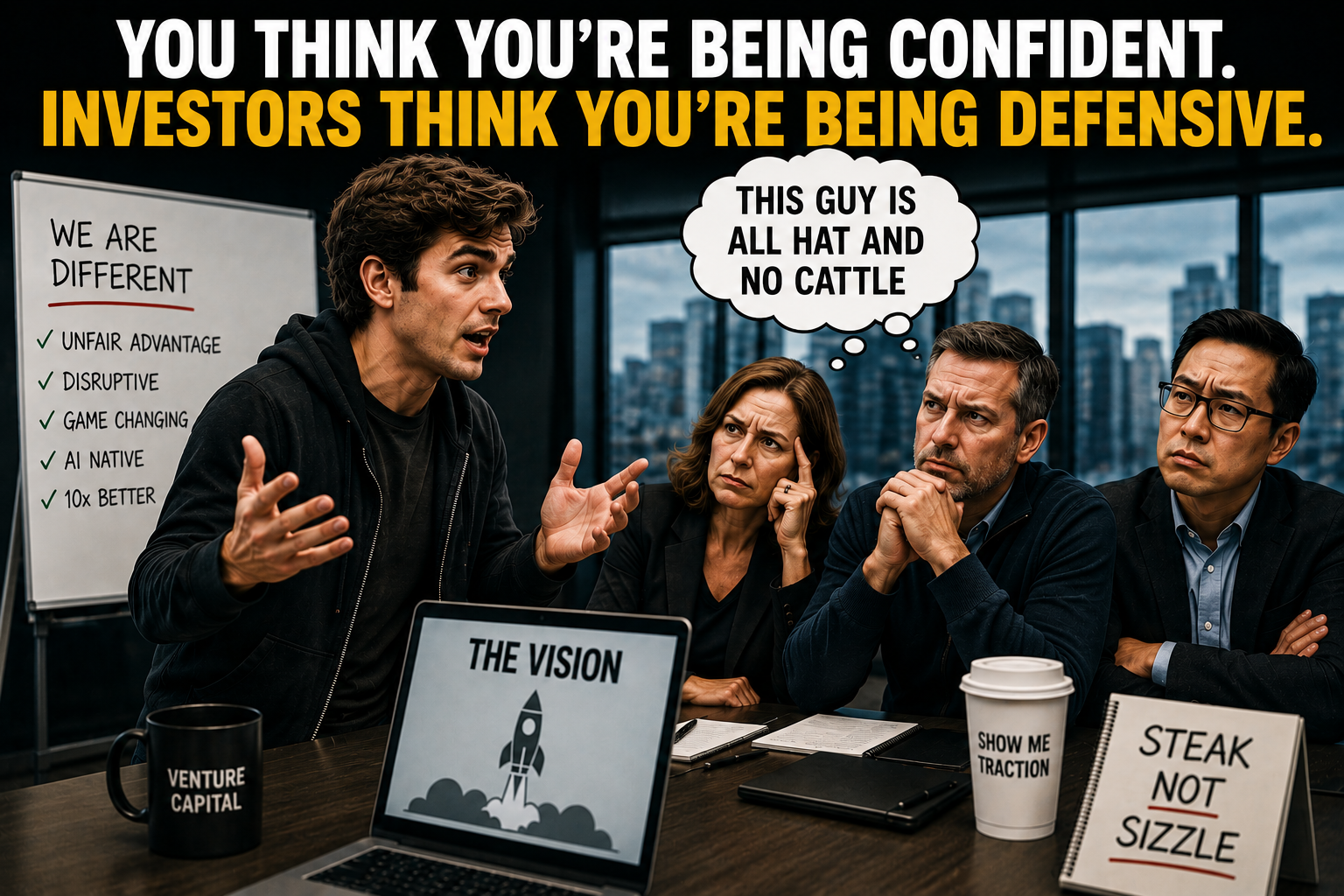

Every founder I have ever coached believes they project confidence. Not a single one walks into a pitch thinking, "I'm going to come across as defensive and brittle today." And yet, investor after investor -- in the feedback sessions, in the post-pitch debriefs, in the quiet conversations that happen after a pass -- says the same thing: "I liked the business. I didn't like the founder's energy."

That gap between what founders think they're projecting and what investors actually perceive is one of the most expensive blind spots in startup fundraising. It doesn't show up in your deck. It doesn't get flagged during pitch prep. It reveals itself in real time, under pressure, in the room.

Here's the part that stings: confidence and defensiveness can look nearly identical from the inside. Both feel like conviction. Both feel like standing your ground. The difference becomes visible only when your ideas are challenged -- which, in every investor meeting worth having, they will be.

Before you say a word, investors are reading you. Not your slides. Not your financials. You.

Seasoned investors have sat across the table from thousands of founders. They have developed pattern recognition that operates below the level of conscious analysis. They are not thinking "that founder crossed their arms, therefore they are defensive." They are sensing something, and the feeling arrives before the explanation does.

Open posture, sustained eye contact, a calm cadence when fielding hard questions -- these are the surface expressions of genuine confidence. They signal that you believe in what you are building without needing anyone else to confirm it. Closed posture, quick pivots away from uncomfortable topics, the slight edge that enters your voice when a question lands somewhere painful -- these signal something different. They signal a founder who is protecting something rather than sharing something.

The trap is that both behaviors feel like strength from the inside. Defensiveness rarely feels like defensiveness. It feels like defending what you know to be true.

Here is the distinction that matters. Confident founders treat investor questions as information. Defensive founders treat them as attacks.

When a confident founder hears "I'm not sure your TAM estimate holds up," they hear an invitation to either sharpen the argument or acknowledge the gap. When a defensive founder hears the same thing, they hear a challenge to their competence and begin marshaling evidence to win the argument.

The irony is that investors are rarely trying to catch you. When they push on your TAM, your churn assumptions, your competitive moat -- that is usually a sign of interest, not skepticism. The hard question is the one they are engaged enough to ask. The founders who misread investor curiosity as hostility are the ones who most often talk their way out of a term sheet.

Three patterns separate the confident from the defensive:

Confident founders welcome the question they don't know the answer to. "That's an area we're still pressure-testing" is not a weakness. It is evidence that you understand your own unknowns, which is far more reassuring to an investor than false certainty. Defensive founders over-explain, reframe the question, or answer a different question entirely -- anything to avoid saying "I don't know yet."

Confident founders acknowledge risk without flinching. Research from HBR confirms what good investors already knew: founders who candidly named setbacks and acknowledged real risks actually secured funding more often, at better terms, than founders who presented an unbroken picture of strength. Admitting what you haven't solved signals intellectual honesty. Pretending you've solved everything signals delusion.

Confident founders can disagree without escalating. If an investor challenges your pricing model and you think they're wrong, you can make your case calmly and then let it sit. You don't need to win the argument in the room. Defensive founders conflate the investor's skepticism with a verdict -- and react accordingly. The moment a founder's voice hardens, their credibility softens.

There is a second distinction that matters just as much, and it lives one degree past confidence: the difference between assertiveness and aggressiveness.

Assertive founders know what they want, state it clearly, and hold their position when it's warranted -- while remaining genuinely open to what the other person is saying. Assertiveness is about communication, not combat.

Aggressive founders use the same energy in a different direction. They dominate the conversation. They interrupt. They answer the question they wish had been asked rather than the one that was. They treat the investor meeting like a courtroom cross-examination, where the goal is to neutralize the other side.

The telltale signal of aggression in an investor meeting is when "I" replaces "we." When one founder is doing all the talking while two co-founders sit silently at the table. When a question about the market gets answered with a monologue about the founder's credentials. Experienced investors notice this immediately. They are not just evaluating the business -- they are evaluating whether this is a person they can work with for the next seven to ten years.

There is a version of energy that works. It is conviction without combativeness. It is a founder who has done the work, knows it, and can demonstrate it calmly -- who can field a contrarian perspective without their nervous system treating it as a threat.

You can be direct, even blunt, without being aggressive. You can hold your ground without making the investor feel like an adversary. The best founders I have seen in investor meetings have a quality I can only describe as settled. They are not performing confidence. They are just confident, which reads completely differently.

After decades on both sides of the table, I can tell you what moves experienced investors more than most founders realize: they are evaluating your behavior under pressure as a proxy for how you will run the company.

The way you handle a challenge in a pitch meeting is a preview of how you will handle a challenge with a customer, a key hire, a pivot, a board member who disagrees with you. Investors are making a bet on future behavior, and your demeanor in the room is the closest real-time data they have.

Coachability is one of the most undervalued signals in early-stage investing. A founder who can absorb feedback in real time, consider it genuinely, and respond without collapsing or hardening -- that founder is going to be easier to back through the inevitable rough patches ahead.

The founders who lose the room are almost always the ones who feel the need to be right. The ones who win it are the ones who feel comfortable not knowing everything, saying so, and focusing instead on what they do know and why it matters.

If you are preparing for investor meetings, here are the behaviors worth practicing -- not in a mirror, but in real conversations with people willing to push back hard.

1. Pause before you answer. The instinct to respond immediately to a challenging question is almost always a defensive one. A two-second pause signals that you are actually thinking about what was asked, not just activating a pre-loaded rebuttal. It reads as confidence.

2. Acknowledge the question before you answer it. "That is a fair question" or "We have wrestled with that" tells the investor their concern registered. Defensive founders often skip straight to the answer in a way that feels like dismissal.

3. Know the three hardest questions about your business -- and answer them first. If you know your customer acquisition cost assumptions are aggressive, name that before the investor does. Owning your vulnerabilities is not weakness. It is control. The investor who surfaces a risk you already know about leaves the room more impressed than the investor who surfaces a risk that surprises you.

4. Let the investor finish. Interrupting is the most common form of aggression in pitch meetings and the most underestimated. Even if you know where the question is going, let it land. The pause before your answer costs you nothing. The interruption costs you more than you know.

5. Separate your identity from your company. This is the hardest one. When you have poured everything into a business, criticism of the business can feel personal. But investors who challenge your assumptions are doing you a favor. The founders who absorb that feedback and act on it are the ones who build better companies. The ones who cannot separate the two are fragile in ways that become very expensive very fast.

Investors do not fund companies. They fund founders -- and they make that decision partly on what the deck says and mostly on who they see across the table.

Confidence is not the absence of doubt. It is the ability to engage with doubt without being destabilized by it. The founders who carry that quality into the room tend to get the meetings. The ones who hold it through the hard questions tend to get the term sheets.

Assertiveness is not the same as aggressiveness. One makes an investor want to work with you. The other makes them wonder who else on your team they should be talking to.

The line between the two is finer than most founders think. The good news is that it is learnable -- but only if you know it exists.